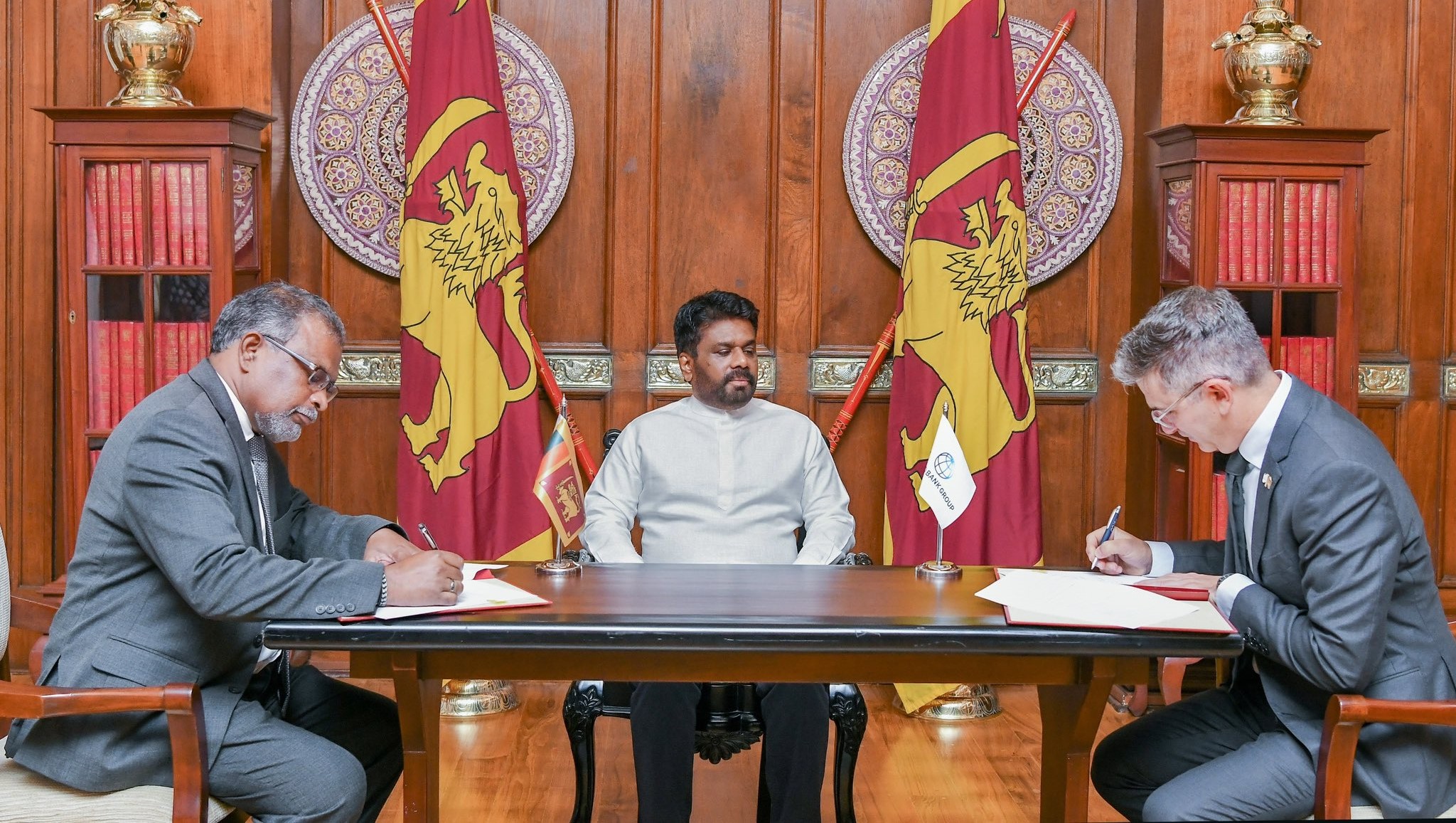

Following the election of Anura Kumara Dissanayake, Sri Lanka has secured a $200 million loan from the World Bank as part of the second instalment of the World Bank’s Resilience, Stability, and Economic Turnaround (RESET) Development Policy Operation (DPO).

Since his ascendancy to the presidency, Dissanayake has made overtures to both the West and India despite his party’s past firmly held anti-Indian opposition. The agreement with the World Bank also follows discussions with the International Monetary Fund (IMF), where the IMF warned that certain “vulnerabilities and uncertainties do remain”.

During his presidential campaign, Dissanayake pledged to “renegotiate” a much-needed IMF bailout program, with fears his pledge could potentially plunging the country back into the economic crisis it experienced in 2022.

According to a statement from the President's office, despite his campaign pledges, Dissanayake “reaffirmed the government’s broad agreement in principle with the objectives of the IMF programme but emphasized the importance of achieving these objectives through alternative means that relieves the burden off the people”.

The first portion of the World Bank’s loan under RESET DPO, totalling $500 million, was disbursed in two phases between June and December 2023. The RESET initiative is designed to support Sri Lanka’s ongoing recovery by enhancing economic governance, boosting competitiveness, and protecting vulnerable communities.

David Sislen, World Bank Regional Country Director for Maldives, Nepal, and Sri Lanka, emphasized the importance of this support:

“Sri Lanka will now have the opportunity to focus on maintaining its hard-earned stability and investing in the private sector to transform the national growth trajectory. Doing so is vital to boosting economic growth, creating jobs, and ensuring that everyone benefits from a stronger, more resilient economy.”

The agreement will see Sri Lanka introduce a range of reforms, including a new Public Debt Management Act which will inform borrowing decisions. Other reforms include amendments to the tax system and tighter regulations on financial sector risks. Additionally, changes to the Telecommunications and Electricity Acts aim to improve service quality and promote export competitiveness by lowering customs duties and phasing out para-tariffs.

The World Bank further reports that a focus of the loan is on enhancing women’s empowerment and reducing gender discrimination.

Read more here.